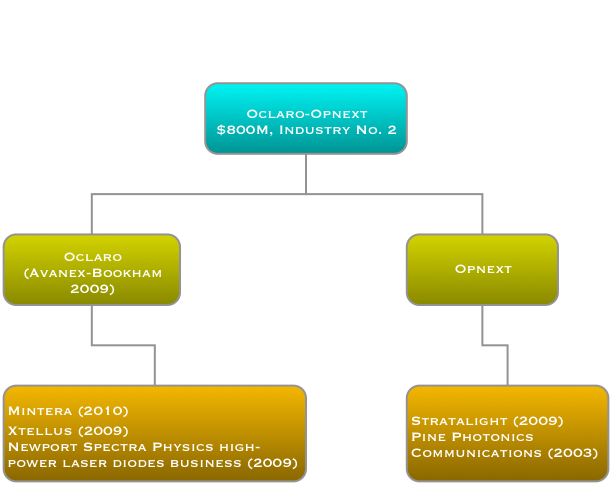

Oclaro-Opnext merger will create second largest optical component company

Oclaro has announced its plan to merge with Opnext. The deal, valued at US $177M, will result in Opnext's shareholders owning 42% of the combined company. The merger of the fifth and sixth largest optical component players, according to Ovum, will create a company with annual revenues of $800M, second only to Finisar. The deal is expected to be completed in the next 3-6 months.

Source: Gazettabyte

Source: Gazettabyte

Other details of the merger include:

- Combining the two companies will save between $35M-45M but will take 18 months to achieve.

- Restructuring and system integration will cost $20M-$30M.

- All five of the new company's fabs will be kept. The fabs are viewed as key assets.

- The new company will continue its use of contract manufacturers in Asia. Oclaro announced a recent deal with Venture, and that included the possibility of an Oclaro-Opnext merger.

- Oclaro's CEO, Alain Couder, will become the CEO of the new company. Harry Bosco, Opnext's CEO, will join the company's board of directors, made up of six Oclaro and four Opnext members.

- In 4Q 2011, Oclaro reported three customers, each accounting for greater than 10% sales: Fujitsu, Infinera and Ciena. Opnext reported 43% of its sales to Cisco Systems and Hitachi in the same period.

Industry scale

The motivation for the merger is to achieve industry scale, says Oclaro. "We have never been shy [of mergers and acquisitions] - we did Avanex and Bookham," says Yves LeMaitre, chief marketing officer for Oclaro. "We believe industry scale allows you to absorb certain fixed costs like fab infrastructure and the sales force." Scale also increases the absolute amount that can be invested in R&D, estimated at 12-13% of its revenues.

"It [the acquisition] is really about building a company that directly competes with Finisar," says Daryl Inniss, practice leader, components at Ovum. "It creates a stronger, vertically integrated company that starts at chips and goes all the way to the line card."

"We will be one of the most vertically integrated suppliers for 100 Gigabit coherent technology"

Mike Chan, Opnext

LightCounting believes the Oclaro-Opnext merger will be a success. Moreover, the market research firm expects further optical component M&As. Since the Oclaro-Opnext was announced, Sumitomo Electric Device Innovations has announced it will acquire Emcore's VCSEL and associated transceiver technology for $17M.

Meanwhile, Morgan Stanley Research is less positive about the merger, believing that the Opnext acquisition carries 'material risk'. It argues that the stated synergies are aggressive and that the integration of the two firms could distract Oclaro and lower its share price.

Products and technology

The deal expands Oclaro's transceiver portfolio, enhancing its offerings in telecom and strengthening its presence in datacom. It also expands the customer base: Opnext supplies Juniper, Google and H-P, new customers for Oclaro.

Common products shared by the two firms are limited, for high-end products the overlap is mainly 100 Gigabit coherent and tunable laser XFPs. LightCounting also points out that the two share some legacy SONET/SDH, WDM and Ethernet products: "Nothing that reduces competition significantly," it says in a research note.

"[With the Avanex-Bookham merger] There was a little bit of overlap in a few areas which we managed," says Oclaro's LeMaitre. "It is even easier in this case."

"We see potential, further down the road, for new very-short-reach optical interfaces"

Yves LeMaitre, Oclaro

Opnext acquired optical transmission subsystem vendor StrataLight in 2009 while Oclaro acquired Mintera in 2010. Both Oclaro and Opnext have used the expertise of the two subsystem vendors to become early market entrants of 100 Gigabit 168-pin multi-source modules.

But Oclaro makes the optical components for the modules - tunable lasers, lithium niobate modulators and integrated coherent transceivers - items that Opnext has to buy for its 100 Gig coherent module, says Ovum's Inniss: "Opnext has built decent gross margins when you consider that a lot of the optics they don't own themselves.” Oclaro's components will be used within Opnext's modules.

"We will be one of the most vertically integrated suppliers for key 100 Gigabit coherent technology moving forward," says Mike Chan, executive vice president of business development and marketing at Opnext.

Opnext stresses that it has its own programmes for integrated photonics. "We have been telling our customers that we have been working on some of these integrated photonics [for 100G coherent]," says Chan. "The StrataLight portion of Opnext also has a lot of work done, and IP created, in the coherent modem area."

Currently both companies' 100 Gigabit modules use NEL's coherent receiver DSP-ASIC. Oclaro has also made an investment in coherent chip start-up, ClariPhy. But for future coherent adaptive-rate designs, the joint company will be able to develop its own coherent chip. "We have the in-house know-how for the coherent modem chip," says Chan.

The merged company is well positioned to address client-side 100 Gigabit-ber-second (Gbps) transceivers. "Here the challenge is to achieve high density and low power [interfaces]," says Chan. Oclaro has VCSEL technology that can be used for very short reach 4x28Gbps arrays. Oclaro says it is the world's leading supplier of VCSELs for a variety of commercial applications and has now shipped over 150M units.

At OFC/NFOEC Opnext demonstrated a 1310nm LISEL (Lens-integrated Surface-Emitting distributed feedback Laser) array operating at 25-40Gbps. The surface-emitting distributed feedback (DFB) laser can also be used for the same 4x28Gbps design, says Chan. "Within the data centre 500m is the sweet-spot," says Chan. "It is not just the physical distance but the link-budget as the signal may have to go through a patch panel." The DFB can be used with multi-mode and single-mode fibre and Opnext believes it can achieve a 1km reach.

Oclaro does not rule out using its VCSEL technology to address such applications as optical engines, connecting racks and for backplanes. "We see potential, further down the road, for new very-short-reach optical interfaces into consumer, backplane, and board-to-board to really expand our addressable market," says LeMaitre

Further mergers

LightCounting argues that the 2011 floods in Thailand have added urgency to industry consolidation, with the Oclaro and Opnext merger being the first of several. Oclaro and Opnext were among the most impacted by the flood with Q4 2011 revenues being down 18% and 38%, respectively, says LightCounting.

Ovum also expects further mergers as companies strengthen their coherent and ROADM technologies.

Inniss believes ROADMs is the next area that Oclaro is likely to strengthen. Oclaro has acquired Xtellus but Ovum says the main ROADM leaders are Finisar, JDS Uniphase and CoAdna. Companies to watch include JDS Uniphase, Fujitsu Optical Components, CoAdna and Sumitomo, says Inniss.

A day after Ovum's and LightCounting's M&A comments, Sumitomo announced the acquisition of Emcore's VCSEL business unit.

Post a Comment

Post a Comment

Reader Comments